In this Mergers & Acquisitions (M&A) Valuation module, we will describe the background for M&A banking that most investment bankers will need to know—particularly from the perspective of valuation. We will cover three key topics:

- M&A Overview

- Building an M&A Model

- Accretion/Dilution Analysis

M&A Overview

There are a variety of ways to value a company. The valuation methods include:

Each of these topics, including Acquisition Comparables, is very important in investment banking and is discussed in a previous module in this training course. In this module, we will concentrate on Merger Analysis, also known as Merger Consequences Analysis.

M&A Background

A merger is the combining (or “pooling”) of two businesses, while an acquisition is the purchase of the ownership of one business by another. Pooling of Interest Accounting, which is how mergers used to be accounted for, is no longer allowed by the Financial Accounting Standards Board (FASB) in the US, and was also disallowed by the International Accounting Standards Board (IASB) for international companies. As a result, M&A transactions must now be accounted for using the Acquisition Method of Accounting (a slightly revised version of the Purchase Method of Accounting). This all can be very confusing, because the word “Mergers” is frequently used to describe either type of combination of two business, but all combinations must now be treated as the purchase of one company by another (in other words, as “Acquisitions”).

Regardless, M&A banking involves analysis for scenarios in which one company (the Buyer) proposes to offer cash or its own common stock in order to purchase the common stock of another company (the Seller or the Target). M&A typically requires the target company’s Board of Directors and its shareholders’ approval (except in the case of a Hostile Takeover, in which one company acquires enough stock in another company to control it, against the wishes of the target’s management and/or shareholders).

Reasons for Pursuing M&A

M&A is a corporate strategy that may increase value for the acquirer by creating an important value driver known as Synergies (ways to increase profit/earnings through an acquisition), among other reasons. Synergies can arise from an M&A transaction for a variety of reasons:

- Increase and diversify sources of revenue by the acquisition of new and complementary product and service offerings (Revenue Synergies)

- Increase production capacity through acquisition of workforce and facilities (Operational Synergies)

- Increase market share and economies of scale (Revenue Synergies/Cost Synergies)

- Reduction of financial risk and potentially lower borrowing costs (Financial Synergies)

- Increase operational efficiency and expertise (Operational Synergies/Cost Synergies)

- Increase Research & Development expertise and programs (Operational Synergies/Cost Synergies)

The acquisition of another company may also be defensive in nature. For example, a large company may wish to acquire a small but growing company if the small company has a substantial competitive advantage over the large company, such as an important technology or patent, or superior product offering. This may protect the acquirer from serious competitive consequences, as the small company may over time be able to grow on its own and eat into the large company’s business.

Merger Analysis

Investment bankers put together merger models to analyze the financial profile of two combined companies. The primary goal of the investment banker is to figure out whether the buyer’s earnings per share (EPS) will increase or decrease as a result of the merger. An increase in expected EPS from a merger is called Accretion (and such an acquisition is called an Accretive Acquisition), and a decrease in expected EPS from a merger is called Dilution (and such an acquisition is called a Dilutive Acquisition).

A Merger Consequences Analysis consists of the following key valuation outputs:

- Analysis of Accretion/Dilution and balance sheet impact based on pro forma acquisition results

- Analysis of Synergies

- Type of Consideration offered and how this will impact results (i.e., Cash vs. Stock)

- Goodwill creation and other Balance Sheet adjustments

- Transaction fees

These will all be encapsulated in the M&A Model, discussed in the next section. An investment banker begins to evaluate a potential M&A transaction by referring to a set of questions that will likely include the following:

- Who is the Seller?

- Publicly traded stock, or privately held?

- Insider ownership or sizable public float (i.e., is a large portion of the company’s shares available for sale in the open market)?

- Who are the potential Buyers?

- Strategic Buyer (an existing company able to gain from potential synergies)?

- Financial Sponsor (a Private Equity firm looking to generate an attractive return via a Leveraged Buyout)?

- What is the context of the transaction?

- Privately negotiated sale or auction?

- Hostile or friendly takeover?

- What are the market conditions?

- Acquisition currency (Cash or Equity)?

- Historical premiums paid for Comparable Transactions?

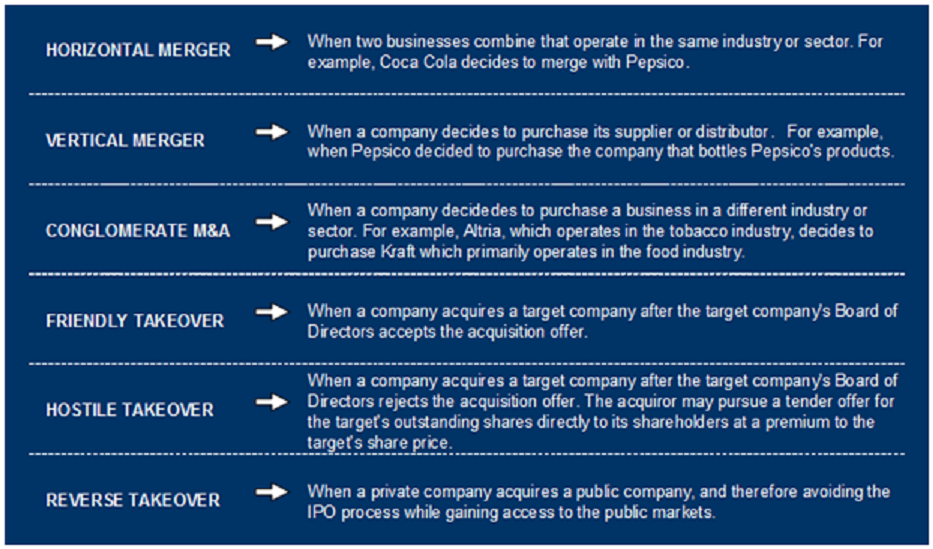

There are also various types of M&A transactions that can occur, both in terms of the dynamics of the transaction and the structuring of it. An M&A banker will need to know all the important distinctions among these types of transactions:

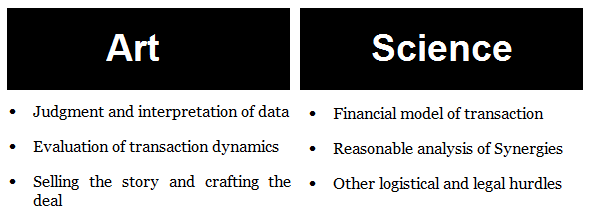

Remember that the M&A Consequences Analysis used by investment bankers is both an art and a science.

Building an M&A Model

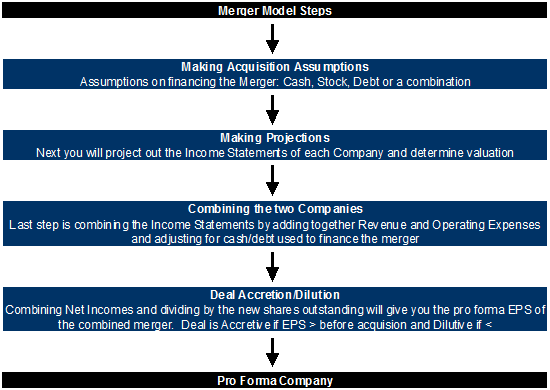

The central piece of the analysis behind M&A advisory services offered by investment banks is the M&A Model. Any junior investment banker involved with a potential M&A transaction will spend many hours building and refining these models! The basic steps to building an M&A Model are as follows:

The Pro Forma Company is the combined entity (the acquirer) after and assuming that the proposed transaction takes place. The differences in the financial attributes of this Pro Forma Company relative to the acquirer itself (before the transaction) will be a key part of the decision whether to go forward with the proposed transaction (for both the Buyer and Seller).

Determining the Purchase Price and Consideration

The Buyer in an M&A transaction intends to benefit from transaction by increasing the value available to its existing shareholders (otherwise, the shareholders are unlikely to approve it). By acquiring all of the shares of the Target company (or at least enough shares to gain control of it), the buyer is willing to pay a Control Premium. A Control Premium is the price paid above market value for a Target public company in order to gain control of the company. Here is a simple example of the control premium:

Company X offers to acquire Company Y for $50 per share. The current share price of Company Y prior to the announcement of the offer price is $40. Therefore, Company X offers a 25% premium over the current market price ($50 ÷ $40 – 1) to gain control of Company Y.

A critical component to evaluating an M&A transaction is to determine the Purchase Price for the Target company. In particular, how much of a Control Premium should be paid for the Target (relative to the current valuation of the target)? One very important method is to look at recent Comparable (Precedent) Transactions to determine how much of a premium has been paid for ownership of other, similar companies in recent M&A transactions. Other methods used to establish a fair value for a target company in an M&A transaction include:

- Comparable Company Analysis

- Discounted Cash Flow Analysis

- Accretion/Dilution Analysis

Typically, all of these valuation methods will be used to value the equity of the target company. These methods will hopefully lead to a reasonable, narrow range of Purchase Prices and Control Premiums for the Target; it will then be up to the management of both the Buyer and Target (along with their respective M&A investment banking advisors) to argue for and agree upon a precise price/premium.

An additional, important issue is the type of consideration being offered to the Seller’s shareholders. The Buyer can offer Cash, Equity (shares of the Buyer’s common stock) or a combination of both as the consideration for the Purchase Price. Which should the Buyer use? Typically, if the Buyer’s current stock price is considered undervalued relative to its peers, the Buyer may decide to not use Equity as consideration, because it would have to give the stockholders of the Target a relatively large number of shares to acquire the company. On the flip side, the Target shareholders may want to receive Equity consideration in this case, because they might feel it is more valuable than receiving Cash.

Conversely, if the Buyer feels that its current stock price is trading at high levels, the Buyer will likely want to use Equity for the consideration of the Purchase Price, because issuing new stock for the transaction is relatively inexpensive (i.e., the stock has a high value in dollar terms). The Target, meanwhile, might be hesitant to receive the Equity as consideration in this case; depending on the terms of the deal, the Seller’s shareholders may end up suffering a loss on the sale relative to Cash consideration in the event that the Buyer’s stock price falls between the time that the deal is announced and the time that the acquisition is completed (usually several months, but in some cases closing can take as long as a year).

As you can see, finding a combination of consideration that is agreeable to both the Buyer and the Seller is an important part of structuring the deal.

Transaction Assumptions

An important step in building an M&A Model is to make assumptions about important parameters affecting the deal, and as a vital step in determining a feasible range for the Purchase Price/Control Premium:

- Current Share Price & Number of Shares Outstanding for the Buyer

- Current valuation information for the Seller

- Expected Purchase Price/Control Premium for the Seller in the proposed transaction

- Portion of consideration arising from Equity/Cash

- M&A transaction fees

- Financing Fees from new Equity and/or Debt issuance

- Expected interest rate on new Debt

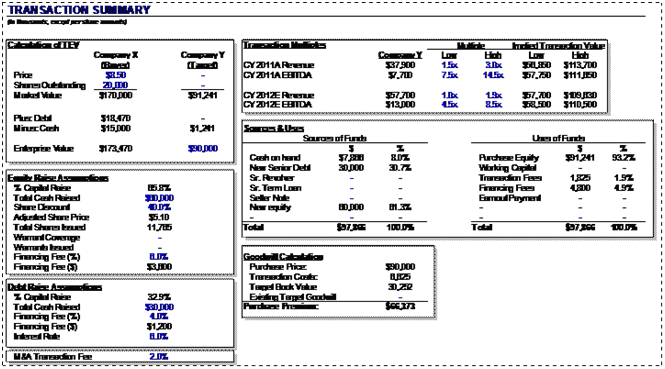

Below is an example of a simple transaction assumptions tab from a M&A Model, in which a Purchase Price range is calculated, as well as an exact, proposed Purchase Price. This proposed Purchase Price will be used in the following sections for discussion.

NOTE: The blue numbers are independent variables or an investment banker’s assumptions. The rest of the numbers are linked to numbers in the model or are calculated from them.

Building the “Sources & Uses” Table

The Sources & Uses section of an M&A Model contains the information regarding flow of funds in an M&A transaction—specifically, where the money is coming from and where it is going.

An investment banker determines the amount of money raised through various equity and debt instruments, as well as from Cash on Hand (i.e., existing Cash owned by the Buyer to help pay for the transaction) to fund the purchase of the Target. This represents the Sources of Funds. The Uses of Funds will show the cash that is going out to purchase the Target, as well as various fees needed to complete the transaction. Importantly, the total Sources of Funds must always balance with the total Uses of Funds.

Using the diagram from the previous section as an example, let’s start with the Sources of Funds side. Assume that Company X, the Buyer, will raise $30 million in New Senior Debt and $60 million in new Equity in order to raise money to purchase the Company Y, the Target company. This will trigger fees for the financing of this Debt and Equity, and these figures are located in the boxes on the left. On the Uses of Funds side, we see that the buyer will purchase the Equity of the target business, which is approximately $91.2 million. M&A transaction fees are 2.0% of the Purchase Price (i.e., the purchase of the Target’s Equity), or approximately $1.8 million. Financing fees include 4.0% of the $30 million in new Senior Debt raised and 6.0% of the $60 million in new Equity raised. These fees will total $1.2 million and $3.6 million, respectively.

Note that the total capital raised is only $90 million. The rest of the money used to pay for the transaction will have to come from Cash on Hand. To get the Sources of Funds to equal the Uses of Funds, we build the following “plug” formula for Cash on Hand:

= (Purchase of Equity + Transaction Fees + Financing Fees) – (Newly Raised Equity + Newly Raised Debt)

Thus, approximately:

= ($91.2 million + $1.8 million + $4.8 million) – ($30 million + $60 million)

= $97.8 million – $90 million = $7.8 million

In this scenario Company X will need to use approximately $7.8 million of Cash from its own Balance Sheet to complete the transaction.

Calculating Goodwill

Goodwill is an asset that arises on an acquiring company’s Balance Sheet whenever it acquires a Target for a price that exceeds the Book Value of Net Tangible Assets (i.e., Total Tangible Assets – Total Liabilities) on the Target’s Balance Sheet. As part of the transaction, some portion of the acquired assets of the Target will often be “written up”—in other words, the value of the assets will be increased upon transaction close. This increase in asset valuation will appear as an increase in Other Intangible Assets on the Buyer’s balance sheet. This will trigger a Deferred Tax Liability, equal to the assumed Tax Rate times the write-up to Other Intangible Assets.

Without getting into too much additional technical detail, here is the formula used to determine the additional Goodwill created in an M&A transaction:

= [Purchase Price of Equity – (Tangible Total Assets – Total Liabilities)] –Write-Up of Assets × (1 – Assumed Tax Rate)

In this case we must add the Transaction Fees and Financing Fees to arrive at the Goodwill figure. Thus, approximately:

Note that in this transaction, Asset Write-Ups are ignored for the sake of simplicity. Here is a detailed technical explanation of Goodwill and other Transaction adjustments, including Asset Write-Ups and Deferred Tax Liabilities.

Note also that Goodwill is a Long-Term Asset but is never depreciated or amortized unless an Impairment is found—in other words, if it is determined that the value of the acquired entity clearly becomes lower than what the original Buyer paid for it. In that case, a portion of the Goodwill will be “written off” as a one-time expense—in other words, the Goodwill asset will be decreased by an amount equal to the amount of the Impairment charge. The write-down of Time Warner’s acquisition of AOL is an extreme, well-known example of such an Impairment charge.

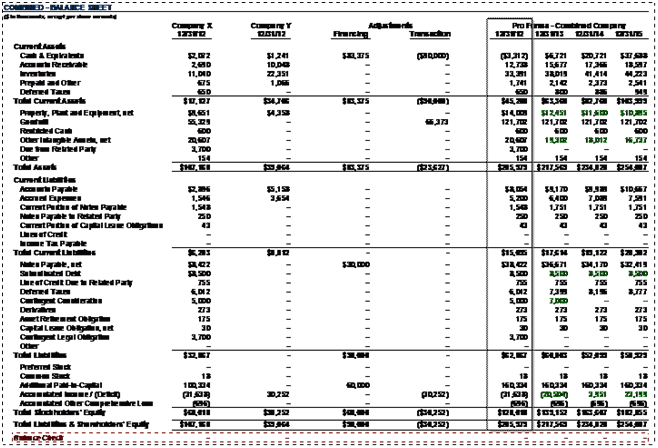

Adjustments to the Pro Forma Balance Sheet

When Company X acquires Company Y, the Balance Sheet Items of Company Y will, for the most part, be added to those of Company X. There will be some adjustments to this, however, and these adjustments must be accounted for. We’ve already discussed one such adjustment: Goodwill. Besides Goodwill, there are additional adjustments that need to be made to the Buyer’s Balance Sheet to account for the transaction. Here is an example of all of the Balance Sheet adjustments that will occur using the adjustments made to the Pro Forma Balance Sheet that reflects the “Transactions Assumptions” illustration given above.

In the illustration above, the adjustments are as follows ($ in thousands):

- Company X, the Buyer, issues $60 million and $30 million in capital. Net of the Equity and Debt financing fees, the Company receives $83,375 in Net Proceeds. Net Proceeds is a financing adjustment that is added to the historical Cash balance. Then the historical cash balance is adjusted for the transaction purchase price of $90,000 (net of the Cash Proceeds of $1,241 on Company Y’s Balance Sheet). Therefore, the cash balance is affected by the following calculation:

Pro Forma Cash & Equivalents = Company X and Company Y Current Cash & Equivalents of $2,072 and $1,241, respectively + $83,375 Financing Adjustment – $90,000 Transaction Adjustment

- The Equity raise of $60,000 is added to the Additional Paid-in Capital and the Debt raise of $30,000 is added to Notes Payable.

- Company Y Book Value is subtracted from the Accumulated Income/(Deficit), also known as Retained Earnings. In other words, the Book Value of Company Y’s Equity is zeroed out.

- Finally, Goodwill is adjusted by the Goodwill amount of $66,373 created in the proposed transaction.

Accretion/Dilution Analysis

After the transaction has closed, the Buyer will own all of the assets, as well as the financial performance (Profit/Loss), of the Target company. Accretion/Dilution Analysis is used to determine how the Target’s financial performance will affect the Buyer’s Earnings Per Share. As we discussed earlier, a transaction is accretive if the buyer’s expected future EPS increases as a result of the acquisition. On the other hand, the transaction would be dilutive if the buyer’s expected future EPS declines as a result of the acquisition. Thus it is important to estimate the Accretion/Dilution potential from a deal before the Buyer can agree to the proposed transaction.

If the consideration used for the acquisition of the Target company is the Buyer’s common stock, the transaction will often be dilutive to the buyer’s EPS due to the fact that the new shares issued to buy the Target will increase the number of outstanding shares of the Buyer. If that is the case, a combination of Equity and Cash may be used to for the consideration of a Purchase Price to minimize the effect of dilution on EPS.

Additionally, an Accretion/Dilution Analysis will attempt to measure the impact of expected Synergies from the transaction (both in terms of increased revenue and decreased costs). Typically these Synergies are represented as a percentage increase/decrease in the Revenue/Costs for the Target’s financial performance, not that of the Buyer.

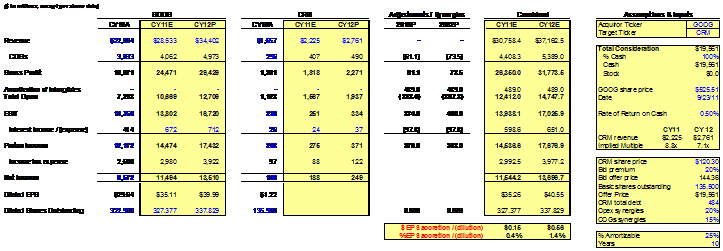

For example, here is a hypothetical accretion/dilution analysis in the event that Google (Ticker: GOOG) had acquired Salesforce.com (Ticker: CRM) in 2011:

The above acquisition scenario assumes 100% consideration in Cash, and once estimates from Synergies are included, the acquisition is accretive to Google’s Earnings Per Share in 2011E and 2012E by $0.15 and $0.56, respectively. (Note that in this scenario Interest Expense increases, because Google would need to issue new Debt to pay Cash for the shares in CRM.)

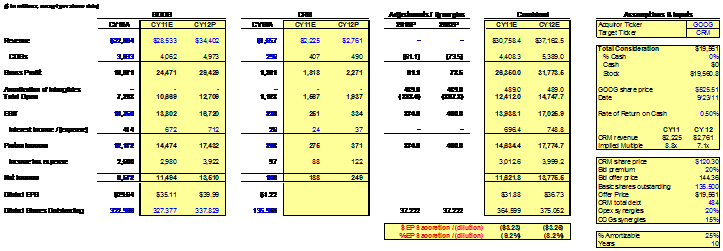

By contrast, the above acquisition scenario assumes 100% Equity consideration. As a result, 37.222 million new shares need to be offered to CRM to fund the Purchase Price; this is dilutive to Google’s Earnings Per Share in 2011E and 2012E by ($3.23) and ($3.26), respectively.

Note that if a Buyer with a relatively low Price/Earnings Ratio acquires a Target company with a relatively high Price/Earnings Ratio, the transaction will generally be dilutive to the Acquirer on a pro forma basis. This is because for each dollar of Price used to acquire the Target company, the Buyer is receiving fewer dollars of Earnings.

Additionally, if the Buyer has an Earnings Yield ([Earnings Per Share ÷ Share Price], or simply [1 ÷ Price/Earnings Ratio]) that is lower than the expected Cost of Debt (the interest rate on new Debt, after accounting for the tax shield from the Debt), then using Equity as consideration will be more accretive (less dilutive) than using Cash. This is because a lower Earnings Ratio necessarily implies a high Price/Earnings Ratio. As a result, the higher the Price/Earnings Ratio of a company, the more likely it is that that company will want to pursue an acquisition strategy, and the more likely it is that that company will want to use Equity as consideration for the deal (all other things being equal, of course).

←Leveraged Buyout AnalysisM&A Case Study: Amazon and Zappos→