Private Equity Investment Professionals

Like investment banks, Private Equity firms typically have a fairly rigid seniority structure with big differences in experience level and responsibilities from top to bottom. In general the senior-most professionals are responsible for deal sourcing, relationship management, and investment decision making, while the junior-most professionals carry the brunt of the analytical workload. However, unlike investment banks, Private Equity firms tend to employ a fairly flat hierarchy structure with fewer layers. This is, at least in part, because Private Equity firms tend to be much smaller than investment banking divisions at major banks. As a result, junior professionals will tend to have much more interaction with senior professionals, fostering much more opportunity to work directly with and learn directly from the most seasoned professionals in the firm.

Here is a brief description of the primary roles in the Private Equity firm hierarchy:

ASSOCIATE: Pre-MBA associates are typically the most junior professionals at the majority of PE firms. The associate handles most of the financial modeling and initial due diligence for investment opportunities, while assisting with the management and monitoring of portfolio companies as well as sourcing deals and supporting transactions. More day-to-day details on the associate’s role are provided later in this guide.

A majority of Pre-MBA associates (especially in the US) are hired for a two-year to three-year program. At the completion of the program, associates are typically expected to attend a top-tier MBA program. Smaller firms will often promote associates to senior associates, and those firms in general tend to provide more opportunities for internal promotions to more senior roles. Such firms include TA Associates and Summit Partners. On the flip side, large LBO firms generally have a more regimented hierarchy and firm structure where the roles are more defined for associates, and where there are limited internal promotion opportunities and limited opportunities to get involved in deal sourcing. Some private equity firms do recruit for private equity analysts out of undergraduate school, although this is uncommon. Most PE hierarchies start at the Pre-MBA associate level, and associates will usually have 2-3 years of prior experience in investment banking or (sometimes) strategy consulting. Firms that do hire analysts straight out of college will offer those analysts roles similar to those of the associates, but the analysts will tend to focus more on logistical tasks, such as participating in conference calls, reviewing data and legal documents, and supporting the associate and vice president with internal investment materials.

VICE PRESIDENT/PRINCIPAL: Vice presidents and principals typically manage the daily responsibilities of the deal teams and work closely with the senior partners of the firm on strategy and negotiations. Professionals in these roles are also expected to generate investment opportunities and potential acquisition ideas. Compensation for a VP or principal varies depending on the size of the PE firm. PE firms will almost always offer some amount of carried interest in the fund to employees at this level.

VPs/Principals manage internal due diligence streams by themselves and have a large role in negotiations. They typically have an MBA degree from a top-tier business school, and one of their main responsibilities is to source investment opportunities by cultivating and maintaining relationships with investment bankers, consultants, and others. VPs/Principals also usually manage the pre-MBA associates and often play a large role in the negotiation aspect of the transaction process.

MANAGING DIRECTOR/PARTNER: Managing directors and partners are the most senior members of the firm and are the ultimate decision makers. They interact directly with the management of portfolio companies, target companies, and investment banks, they conduct negotiations, they source deals, and they deal routinely with the PE firm’s Investment Committee. A typical managing director receives significant compensation in terms of carried interest in the PE fund(s).

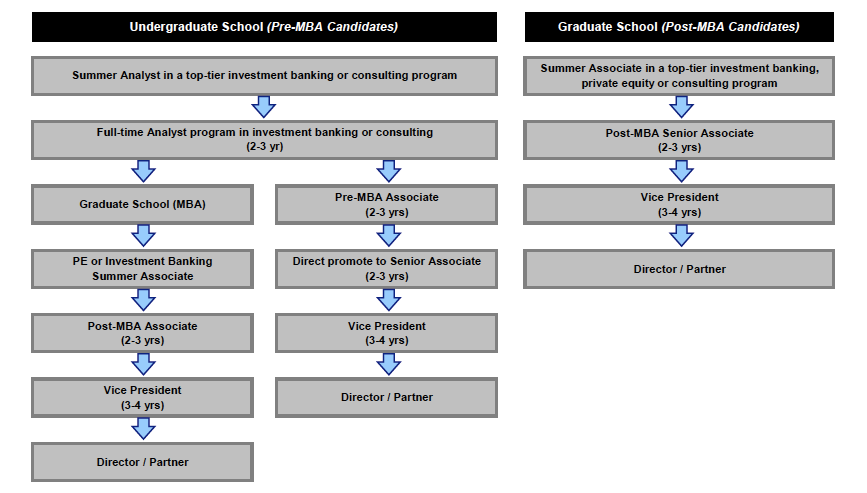

Typical Private Equity Career Path

A typical career path for pre-MBA and post-MBA Private Equity professionals is illustrated below.

Typical Day of a Pre-MBA Investment Associate

Private equity is an extremely complex business, and an associate’s daily responsibilities vary tremendously depending upon the firm the associate works for as well as what stage of the deal process the associate is currently working on. That said, one can paint a fairly broad picture about what an associate’s responsibilities look like overall. Here is a timeline for a “typical workday” for you as a private equity associate:

8:00 a.m.: On the way into the office, you read various news sources, such as the Wall Street Journal or Investor’s Business Daily, and check emails that you received the previous night and this morning to make sure you are prepared to take care of any pressing tasks as early as possible.

8:30 a.m.: You arrive at the office and go through any unaddressed emails. For example, you might see that you have received an investment teaser from a boutique investment bank on a potential sale of a retail chain. Given that you focus on consumer products and that this opportunity fits your fund’s investment criteria, you decide to share the idea with a vice president in your investment area to discuss whether the opportunity is attractive and worth pursuing for further consideration.

9:00 a.m.: You pull up an LBO model template for a different investment opportunity and input a new base-case scenario that a senior member of the investment team would like to review this morning. You have been working on this investment opportunity for the last several weeks and are getting ready to submit a Letter of Intent (First Round Bid) to possibly acquire the relevant business.

11:00 a.m.: You make phone calls to various contacts on the buy-side and on the sell-side to catch up on any news that came out that morning and discuss any new events occurring in the industry or sector you cover.

12:00 p.m.: You catch up over lunch with a former colleague that works at a private equity firm where your firm occasionally co-invests.

1:00 p.m.: You send the updated LBO model to the senior member and meet in his office to discuss your assumptions and the feasibility of the scenario. You notice that the IRR could be optimized using a different debt instrument, and you go back to your office to update.

3:00 p.m.: Given that you received that investment teaser in the morning, you decide to look for relevant sector and comparable company research reports to get a better sense of the available opportunity according to market conditions and research conducted by others.

4:00 p.m.: You receive an email containing the monthly profit & loss (“P&L”) of a portfolio company you are partly responsible for monitoring. You open up the financial model for the company and update the numbers in the model to reflect the actual results you just received and then send the model to the senior member of your investment team who also is responsible for the monitoring of that company.

6:00 p.m.: At the end of the business day, you receive a financial due diligence report for a potential investment that has been approved by your Investment Committee to pursue further into the diligence process. You go through the report and then summarize the findings in an internal memorandum that you have been putting together in preparation for final Investment Committee approval process.

8:30 p.m.: You complete the memorandum and decide to call it a day, have dinner, and go to the gym for a quick workout before heading home.

←Monitoring & Exiting Private Equity InvestmentsPrivate Equity Resume→