The typical process for evaluating and completing a new private equity investment opportunity has many different and structured steps that can vary widely by PE firm, and can differ greatly due to specifics of the target company or the transaction process. The initial investment evaluation can happen very quickly, but the entire process may take several months or even a year or more. The discovery and assessment of the opportunity at the beginning of the process is called “sourcing”—in this phase, the firm locates potential targets and looks at the viability of the investment and the potential returns available. Then, as more information is gathered, the firm conducts due diligence, creates and develops very detailed financial models, and evaluates the pros and cons of the opportunity prior to final approval and execution of the transaction.

Sourcing of an Investment Opportunity

Sourcing for investment opportunities can be difficult and grueling, but it is an essential skill one needs if aspiring to have a successful career in the PE industry. Depending on the PE firm’s preference, a deal may be sourced through a variety of channels: internal analysis, networking, detailed research, and cold-calling executives at attractive companies, for example. Other sources include meeting with various companies, company screens through databases for specific criteria, industry conferences, and conversations with industry consultants and experts. Opportunities sourced through any of these means is referred to as proprietary sourcing—i.e., internally sourced.

Another common way to receive potential investment opportunities is through a financial intermediary, such as an investment banker. Companies often hire investment banks to sell businesses via Confidential Information Memorandums (CIMs), which are distributed to potential acquirers, possibly including both financial sponsors (private equity firms) and strategic buyers. This is typically characterized as a public auction. While searching for potential opportunities, an associate would need to ensure that the investment opportunity fits into the firm’s investment strategy, such as a minimum EBITDA, industry, potential value creation strategy, or a minimum (or maximum) equity check.

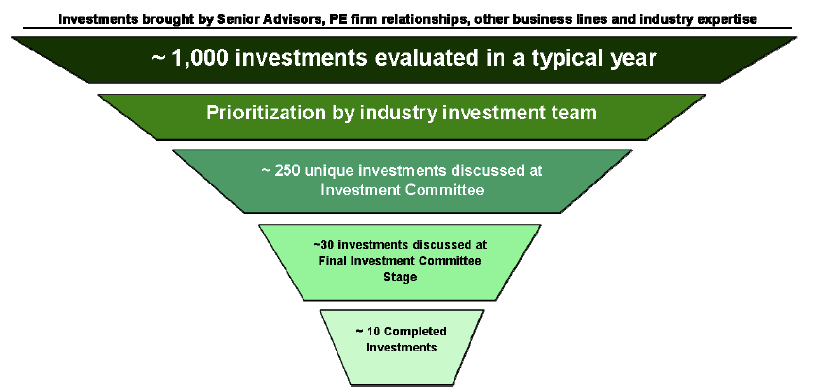

Below we demonstrate the “sourcing funnel” of potential investment opportunities at an illustrative private equity firm:

Investment Process up to Signing

- Signing a Non-Disclosure Agreement (NDA): In a public auction, investment bankers will often send out teasers, which are 1-2 page summaries about the company up for sale. If the investment team finds the teaser interesting, they will negotiate and sign an NDA to receive the company’s CIM prepared by the investment bankers. In a proprietary-sourced opportunity, investment teams will often sign an NDA directly with the target company in order to receive some confidential information regarding the company from management.

- Initial due diligence & Management Presentation: At this stage, the investment teams will perform some initial due diligence to better understand the company. This generally includes research on the industry, talking to advisors about the specific company and the industry, and a building and enhancing a preliminary financial/LBO model using the management’s projections to understand the potential returns of making the investment. At the same time, the investment team may start reaching out to investment banks to hear their thoughts on the company and understand how much debt financing (and what type) would be available for an acquisition of this company. In a public auction, investment bankers will also offer a select group of potential buyers an opportunity to meet with the management team (referred to as a “Management Presentation”). The management team will present an overview of the company while the deal team is allowed to ask them questions about their business. In order to prepare for the management presentation, the investment team will create an initial due diligence question list (similar to questions discussed in the Commercial Due Diligence section).

- Deal Alert (first review with Investment Committee): After reviewing the management’s presentation and having initial discussions, the investment team will prepare a brief (2-3 page) investment proposal and present it to the PE firm’s Investment Committee. The first Investment Committee meeting can have a variety of different purposes, depending on the PE firm. The meeting can be a deal update where no approval is needed, or it can be the beginning of a formal approval process, whereby a deal team will be given permission to submit a First Round Bid (discussed below) and/or a budget to spend a specified amount of money (referred to as “cost cover”) on consultants or other deal-related expenses. If approved, the investment would proceed into further diligence and discussions with the target company and its investment bankers.

- Non-Binding Letter of Intent (LOI) or First Round Bid: At this point, the investment team may present the target company with a non-binding LOI for the transaction on certain criteria that have been shared with the investment team. The offer will detail a proposed purchase price (often a valuation range is given, rather than a specified amount), a proposed capital structure post-acquisition, key assumptions made, key due diligence areas, approximate timing needed to submit a binding offer, the PE firm’s relevant expertise and experience, and the necessary authorizations & approvals required by the PE firm’s Investment Committee in order to complete the transaction. At this point, the target company and its investment banking advisors will generally choose a few bidders to move on to the next round in the auction process. The seller will base its decision on key considerations, including total purchase price, credibility of the offer, the submitting firm’s experience and value creation strategy, and the submitting firm’s compatibility with the current management team.

- Further due diligence with management: The target company will begin providing more detailed confidential information in what is typically referred to as a virtual dataroom to the bidders that proceed beyond the first round. Some example dataroom files are the corporation’s organization and legal entities, board minutes and reports, detailed operations records, owned and leased property agreements, intellectual property documentation, employee lists and employment agreements, detailed segment financial information, and historical audited financials. At this point, private equity firms will begin reviewing all of the relevant dataroom files and start to get more specific, detailed questions to the management team. Follow-up due diligence calls will be held (through the supervision of the investment bankers) with specific members of the executive and non-executive management team. Also, based on the dataroom files, the deal team will start brainstorming the critical issues that they will often hire third-party consultants to help investigate.

- Building an Internal Operating Model: After having detailed conversations with the management team on all of the main drivers behind the business, the investment team will start building a detailed operating model for the business based on reasonable forecast assumptions. An operating model is a very detailed revenue and cost breakdown that is based on specific drivers and assumptions (e.g. price, volume, raw material costs, number of branches, number of customers, renewal rates, fixed vs. variable cost structure, etc.). All of these breakdowns combine into one model to describe the expected financial performance of the company in great detail. This gives the PE investors more detail on the drivers of potential return for the acquisition.

- Preliminary Investment Memorandum: Once the team has completed a more detailed investment model, and a comprehensive investment thesis (reason for investing) and strategy (plan to carry out the investment thesis), a Preliminary Investment Memorandum (PIM, typically 30-40 pages) is compiled to summarize the investment opportunity to the Investment Committee. Sections in the PIM typically include:

- Executive Summary: Details of the proposed transaction, background, and overall deal team recommendation and investment thesis.

- Company Overview: History, description, products & applications, customers, suppliers, competitors, organizational structure, management team biographies, etc.

- Market and Industry Overview: Key market growth rates, trends, etc.

- Financial Overview: Historical and projected income statement, balance sheet, and cash flow statement analysis.

- Risks and Key Areas of Due Diligence: Potential risks to the industry/business and key areas of completed and ongoing due diligence.

- Valuation Overview: Comparable company analysis, precedent M&A transactions analysis, DCF analysis, LBO analysis, etc.

- Exit: Initial thoughts on investment exit options and anticipated timing of exit.

- Recommendations and Proposed Project Plan: The deal team will recommend proceeding with their proposed project plan based on a specific valuation range and budget approved by the Investment Committee. The project plan will include the hiring of third-party consultants to perform commercial, financial, and legal due diligence, and the team will hold further discussions with potential debt and mezzanine financing providers. Deal teams will typically perform only initial legal due diligence at this stage, since it is the most costly, and will typically hold off on it as long as possible (usually until the final stages of the bidding process).

- Final Due Diligence and process up to submit a binding bid: Provided that the PIM has been accepted by the PE firm’s Investment Committee, the investment deal team and its consultants will perform any and all final and confirmatory due diligence in order to provide a Final Binding Bid for the target company (discussed later). At this stage, the deal team is now working exclusively on this investment opportunity (other potential investments that the PE professionals on the deal team were working on will be put aside or farmed out to other PE professionals at the firm) and is having daily interactions with the seller’s investment bankers and management team. The bidder will send specific requests to the company based on all key outstanding issues. These could include site visit requests, calls with specific salespeople/non-executive management, or calls with customers and suppliers. In addition, the deal team will be managing its consultants on other due diligence work streams, including portions of the commercial, financial, and legal due diligence process (detailed in “Areas of Due Diligence”). For example, management consultants (McKinsey, Bain, BCG, etc.) are typically hired to perform commercial due diligence on the addressable market, trends, and customer relationships. Accountants (KPMG, PricewaterhouseCoopers, Ernst & Young, Deloitte, etc.), specifically within the Transaction Services group of the accounting firm, are hired to perform confirmatory financial due diligence to ensure that all the financial information provided is accurate. M&A lawyers (Wachtell Lipton Rosen & Katz, Skadden, Sullivan & Cromwell, Simpson Thacher, etc.) are hired to perform legal due diligence and to handle the initial drafting of acquisition documents. At the same time, the investment deal team will be negotiating with the financing banks on the debt financing terms. When negotiating, the deal team’s objective is to obtain the best debt financing execution (i.e. choosing the right group of banks) at the most favorable debt terms. The deal team will also assist the financing banks with their own due diligence by fielding their specific questions and concerns in order to get them more comfortable with underwriting their debt commitment. The average time for this entire confirmatory due diligence process (occurring between the First Round Bid and the Final Binding Bid) is approximately 3 to 6 weeks.

- Update and Final Investment Committee Approval: Depending upon the exact investment process of the private equity firm, an investment deal team must update the Investment Committee on key deal issues in a number of potential ways. Once all due diligence items are completed and the investment team is comfortable moving forward, a Final Investment Memorandum (FIM) is completed. A FIM is essentially the equivalent of a PIM (which was completed before the First Round Bid) that also includes further due diligence from the deal team and third-party consultants, and specifically addresses the key issues introduced by the Investment Committee from the PIM. At this stage, the deal team will recommend acquiring the target company at a specific valuation, which the Investment Committee will either reject or approve. It is very common for private equity firms to proceed beyond the first round without submitting a final binding bid or being restricted to a maximum price by the Investment Committee (i.e., they will not able to raise their price or indicative valuation range, or may even fall short of the range specified in the First Round Bid).

- Final Binding Bid and Signing: If it receives approval, the investment deal team will submit a Final Round Bid (or Final Binding Bid) for the target company. This final bid is almost always binding (i.e. all due diligence has been completed) and includes a final purchase price, fully-committed financing documents from investment banks, and marked-up preliminary merger agreements to be discussed with the seller’s lawyers. The seller and its investment bankers will spend a few days discussing the various final bids and will choose a winner. They will then work exclusively (and often exhaustingly!) with that bidder in order to sign the transaction. Once a winner has been chosen, negotiations between the lawyers of the seller and the lawyers of the buyer will continue to finalize the Merger Agreement (also referred to as the Purchase Agreement) and other related transaction documents. Several key points in the Merger Agreement will be negotiated, and the most important of those is the Purchase Price Consideration (i.e., the definition of what is to be subtracted from the Purchase Price to calculate the total amount wired to the Seller’s stakeholders). Additionally, the Merger Agreement will spell out logistics of the wire transfers to equity (and other) stakeholders, and how much is to be withheld for post-transaction adjustments.

Investment Process from Signing to Closing

Once a private equity firm has officially signed a deal with the target company, both parties will jointly issue a press release announcing the transaction. From there, both parties will work toward closing the transaction, which can take from a few months to a year to complete, depending on the size and complexity of the transaction. At this point, the seller’s investment bankers will become less involved, and the main interactions will be between the lawyers representing the buyer and seller.

- Management Equity Roll-Over and Incentive Option Pool: Depending on whether the private equity firm wants to keep the current management team, it will start negotiating with the executives on their equity roll-over commitment and their incentive option pool. PE firms will work hard to ensure that the management’s interests are well aligned with theirs. Note that if the deal consists of the acquisition of a publicly-traded company, the private equity firm is prohibited from having any discussions with the management team about compensation before the deal is actually signed.

- Execute Debt Financing: Once a deal is signed, all parties involved will start working on marketing materials to present to prospective debt investors. In particular, if the debt markets are active and financing is available at attractive rates, the financial sponsor will try to finalize the debt financing as quickly as possible. The financial sponsor will have negotiated specific debt amounts and interest rates with the financing banks, but the banks will have “flex terms” negotiated into their commitment letters which allow them to adjust the debt terms if the financing markets turn sour (i.e., if the proposed financing terms cease to be viable due to adverse changes in financial market conditions). The transaction closing and the debt financing execution are coordinated with each other, as the debt is a vital part of the transaction funding.

- Closing Funds Flow: Once all the necessary documentation is completed, the private equity firm must ensure that everyone is properly paid on time, including selling equityholders, existing debtors, target and acquirer advisors, and the escrow agent. Since transactions can reach billions of dollars in size, this part of the process can be very difficult to navigate, given the numerous parties involved, various ownership structures, multiple funding sources, and complicated funding timelines.