In this Precedent Transaction Analysis chapter, we will cover five key topics:

- Precedent Transaction Analysis Overview

- Peer Universe for Precedent Transactions

- Calculating a Precedent Transaction Multiple

- Price Premium Analysis Overview

- Common Mistakes

Precedent Transaction Analysis Overview

What are Precedent Transactions?

Precedent Transaction Analysis, also known as “M&A Comps,” “Comparable Transactions,” or “Deal Comps,” uses previously completed mergers and acquisitions deals involving similar companies to value a business.

Precedent Transaction Analysis typically uses the same multiples as Comparable Companies’ Analysis (or “Comps”). In particular, Enterprise Value/Sales, Enterprise Value/EBITDA and Earnings/Earnings Per Share (EPS) are the most commonly used metrics. However, unlike in Comparable Company Analysis, the basis for value comparison is the price paid by the purchaser for a business, rather than the traded market values of the company’s securities. These prices can be different because there is a control premium—the value ascribed to being able to control a business rather than simply own a percentage of the equity in it. Thus, Precedent Transaction Analysis will typically result in valuations that are higher than standard Comparable Company Analysis.

Additionally, Precedent Transaction Analysis tends to focus on the value of a business as of the time an acquisition of the business can be completed, rather than today. This is because deals take time to close, whereas current market values for a business can be assessed on any day. Sometimes, deals can take as long as a year (or more!) to close, so the Precedent Transaction Analysis should reflect that fact.

For all of these reasons, Precedent Transaction Analysis should be part of the valuation analysis of any company in which a change of control (such as via an acquisition) is possible.

Below you will find a detailed overview of Precedent Transactions techniques used by investment bankers and leveraged buyout investors (also known as “financial sponsors”) to value a company.

Why Use Precedent Transactions?

There are many reasons why a Precedent Transaction Analysis should be used as part of a valuation exercise:

- To value a private business that does not have public trading comparables.

- To evaluate the market demand for acquiring a company, based on the total dollar volume and number of recent transactions in a certain industry.

- To provide data analytics in assessing M&A activity and consolidation trends.

- To identify potential bidders if the company is looking to be acquired or identify potential sellers if a company is looking to buy a business.

- To provide a fairness opinion to a Board of Directors when a company is acquiring or selling all or part of a business, or is being acquired.

Precedent Transactions Advantages and Disadvantages

|

PROs and CONs of Using Precedent Transactions

|

|

|

PROs

|

CONs

|

|

|

Peer Universe for Precedent Transactions

Searching for Precedent Transactions

Information on Precedent Transactions can typically be found in a number of places:

- Previous valuation analyses: A great source for previous transactions is presentation material that has previously been compiled in a certain industry. This can be a great way to save time, so be sure to check whether such analyses have recently been conducted at your bank—chances are high that they have.

- Public tender documents and merger proxy statements: Fairness opinions disclosed in public tender documents and merger proxy statements can provide a wealth of information about other closed transactions.

- SDC database: Securities Data Corporation compiles a database of all completed M&A transactions and can be used to search for relevant transactions.

- Capital IQ or Factset: This database is a widely used internet-access financial database that has a search feature for M&A transactions that can be filtered by many factors including target company geography, size, etc.

- News internet searches: Try a Google search for industry M&A news.

- Equity research: Typically transaction information can be found in initiation reports.

It is important to note that primary sources are always the best source of information regarding M&A multiples. We suggest using information that is disclosed directly by a company, such as a merger proxy statement. Documents available via the SEC should be close in quality to primary documents, because the SEC is where public companies disclose press releases and all major corporate and financial events. Also valuable are Equity Research reports, if they are cross-verified by company press releases and proxy statements. By contrast, multiples available from databases such as SDC, Capital IQ and Factset may need to be verified.

Selecting the Appropriate Precedent Transactions

The appropriate selection of a relevant peer universe is critical for a Precedent Transaction Analysis, because it plays a significant role in the valuation of the company, when viewed as a potential M&A target. For example, a company could sometimes be compared across two different industries due to the nature of the business (e.g. an internet retail company). This will affect which comparable transactions to use. Similarly, some comparable transactions might need to be ruled out or adjusted because of specific transaction dynamics. Finding the right Precedent Transaction Peer Universe can therefore be somewhat subjective.

The best Precedent Transactions to use are those in which the target companies and the company you are valuing have the most similar business and financial characteristics. These characteristics include the following:

- Same business & industry

- Similar business size

- Similar sales growth rates and profitability margins

- Similar capital structure

- Similar reasons for transaction (e.g. fire sale, bankruptcy, or strategic motive).

- Same geographic location of operations

The best way to get a relevant set of Precedent M&A transactions is to go to one relevant example transaction and search for the Fairness Opinion filed in a target company’s Merger Proxy (filed with the SEC under Form S-4). That Fairness Opinion should include a robust set of relevant transactions that are similar to the one disclosed in the S-4 document.

For example, let’s assume that we are looking for comparables to a company that conducts its business in the cloud-computing sector. In 2011, Time Warner Cable acquired NaviSite, a cloud-computing business, for approximately $230 million. The relevant transaction filing can be found on the SEC website.

In this document, we can search for the fairness opinion conducted by Raymond James & Associate using the search text “Selected Transaction Analysis.” Raymond James states the following:

“While none of the companies (other than the Company) that participated in the selected transactions are directly comparable to the Company, the companies that participated in the selected transactions are companies with operations that, for the purposes of this analysis, may be considered similar to certain operations of the Company. Raymond James excluded transactions whose targets may have offered services similar to those of the Company, but that also derived a large part of their revenues from businesses dissimilar to those of the Company.”

Just prior to this quote, the Raymond James analysis provides a relevant set of 15 comparable transactions to help get us started.

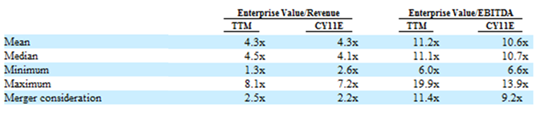

Based on the set of transactions listed in the proxy statement, Raymond James concluded that the Precedent Transactions multiples were as follows:

From the analysis summary, Raymond James demonstrates that the merger consideration for the NaviSite acquisition is relatively close to the average multiples of the selected transactions, if measured in terms of Enterprise Value/EBITDA. In terms of Enterprise Value/Revenue, the consideration is on the low side—but the implication is that NaviSite has a low EBITDA margin relative to the universe of companies used in this analysis.

Calculating a Precedent Transaction Multiple

Let’s take a look at a completed precedent transaction and determine the relevant multiples for that transaction. The key information to be gathered includes the following:

- Announcement date

- Target and acquirer name

- Consideration type (cash or stock)

- Equity Value (based on offer share price and diluted shares outstanding)

- Enterprise Value (based on equity value plus net debt)

- LTM financial results of the target

The example we will use is the acquisition of J.Crew Group for $43.50 per share in cash by TPG Capital and Leonard Green & Partners. The press release states, “The price represents a premium of 29% to J.Crew’s average closing share price over the last month.” From the press release and supporting SEC filings, we can gather and compute the key information described above.

The first step is to calculate the market value of J.Crew prior to the announcement. There were 63.741 million basic shares outstanding prior to the announcement, according to SEC filings. This document shows that the company had approximately 7.977 million options outstanding. Therefore, we can assume the diluted share count equals 63.741 + 7.977 = 71.718 million. For the equity value of J.Crew, we use the offer price times the dilutive shares outstanding. Therefore, J.Crew’s implied Equity Value is [71.718 million × $43.50] = $3,120 million.

Next, we calculate the implied enterprise value, or total consideration, by taking the equity value and adding total debt balance minus total cash and short- term investments. According to the 10-Q filing, J.Crew had $340.5 million in cash and $49.2 million in total debt as of July 31, 2010. Thus, J.Crew’s implied Enterprise Value is therefore [$3,120 + $49.2 – $340.5] million = $2,828 million.

Finally, we can gather the Last Twelve Months (LTM) financial data from J.Crew’s SEC filings. A review of these documents shows that J.Crew’s LTM revenue was $1.711 billion and its LTM EBITDA was $320.78 million. From this data, we can calculate the following multiples for this Precedent Transaction:

In addition to the historical acquisition multiples, investment bankers use research reports that were published prior to the announcement of the deal (this is very important) to get a sense of projected financial performance estimates. From these, we can compute what forward/estimated acquisition multiples were used. For example, if J.Crew was expected to have revenue of $2.5 billion in 2011, then we can assume that the 2011E EV/Revenue multiple for the transaction was 1.1x.

This procedure can be repeated for each relevation transaction in the Peer Universe. Once this is completed, aggregate statistics for the multiples should be presented (minimum, median, mean and maximum).

An example analysis would look something like this:

Additional points to note as you are performing a Precedent Transaction Analysis include the following:

- Enterprise Value = Equity Value + Total Debt – Cash + Minority Interest + Preferred Equity.

- Calculate LTM financial performance based on latest filings prior to announcement.

- Determine projected financial performance by using a recent research report published prior to announcement.

- Exclude extraordinary one-time items such as restructuring charges. Make sure to footnote any such exclusions.

- Look for convertible securities that may convert upon change of control of the target. These securities will likely be included in the diluted share count.

- Always double-check your work! Cross check research reports, company filings and press releases.

Price Premium Analysis Overview

Investment bankers calculate the control premium of Precedent M&A Transactions to approximate the appropriate offer price premium for a target company. Typically, the difference between the share price one day prior to announcement and the offer price is used. The following is an example of a Precedent Transaction Analysis that included Price Premium data:

The formula for Premium Paid (as a percentage above market) is:

Where “Last Trading Price” is generally the closing price of the stock the day before the acquisition announcement is made.

For example, if Company A last traded at $100 per share upon Wednesday’s close, and Company B announces its intent to acquire Company A for $125 per share on Wednesday evening, Company B is paying a 25% premium over the market price to gain control of Company A.

In some cases, there are rumors or leaked information regarding potential M&A activity that can manipulate or impact the trading price of a potential target company’s stock price. Therefore, investment bankers can also perform a price premium analysis relative to the price one week or one month prior to announcement.

Pitfalls To Avoid When Using Precedent Transactions

There are a number of common ways that mistakes can be made when performing Precedent Transaction Analysis. Be sure to review this checklist of pitfalls to avoid before completing the analysis:

Inconsistent announcement date or effective transaction date

Always keep your data points consistent. If you are looking at a set of precedent transactions, be sure to use the LTM data points when calculating the respective multiples (rather than, for example, using multiples based upon the prior fiscal year end). Keeping the data points consistent in your analysis will ensure a more consistent valuation. If any data points are not consistent and difficult to make consistent, make sure to footnote them, and at least consider removing them from the aggregate statistics for the analysis.

Including extraordinary items

Make sure to exclude any one-time items from the financial results data. These items may include gains/losses on sales of assets, legal expenses, write-offs or restructuring expenses. Always footnote any exclusion.

Including minority interests in financial results

Any minority interest expense or income should be excluded from the financial data points used to calculate multiples if the minority interest is not related to the company’s core line of business. Always footnote any exclusion.

Taking the numbers straight from an online financial database

It is imperative that you conduct your own research on any given transaction. Financial databases often have inaccurate or imprecise metrics. Try to always use primary sources when possible, as this should help ensure that the data is accurate and appropriately adjusted for extraordinary items.

Failing to calculate the premium over market value

Be sure to calculate the true premium of an offer price – in other words, make sure that the market price prior to the transaction has not been manipulated by market rumors or insider trading. Charting the stock price over the previous six month prior to announcement of the transaction can give you a sense of what the historical price was prior to any possible appreciation immediately prior to announcement caused by information leaks or illicit behavior.

←Discounted Cash Flow AnalysisInitial Public Offerings→